Use these two secret methods to find how much house you can afford

More than 40 million Americans are house poor, living with housing costs they can’t afford. How do you know how much house you can afford and how much is too much?

In this video, I’ll show you two ways to figure out how much house you can afford. Then I’ll reveal a super-savings hack that will save you hundreds a month.

What is House Poor?

According to a new study out of Harvard, almost 40 million Americans live in a house they can’t afford. That number has more than doubled over the last ten years and the median home price surged to over $285,000 last year.

It’s so bad; we even have a word for it. Being ‘House Poor’ is when you have a nice house but the mortgage payments push you beyond your budget. You’re constantly stressed out, trying to skimp every penny to make payments and it’s a path that only leads to bankruptcy.

So can you afford a house and maybe more importantly, how much house can you afford? The banks and real estate agents are no help. They want you to borrow and buy as much as possible.

How Much House Can I Afford?

In this video, I want to show you how much house you can REALLY afford and still be happy, plus how to get the most bang for your buck and stay within your budget.

Let’s first look at how to figure out how much house you can afford without being house poor; then I’ll reveal a secret savings trick that even budget guru Dave Ramsey doesn’t know.

The Rules for How Much House You Can Afford

So the typical rule of thumb is that you can safely spend 28% of your monthly income on housing costs and up to 36% on total debt payments. We’re going to tweak this a little to make it a little safer; I’ll show you how to use the rule then I’ll show you how to turn Dave Ramsey’s advice into that super savings hack.

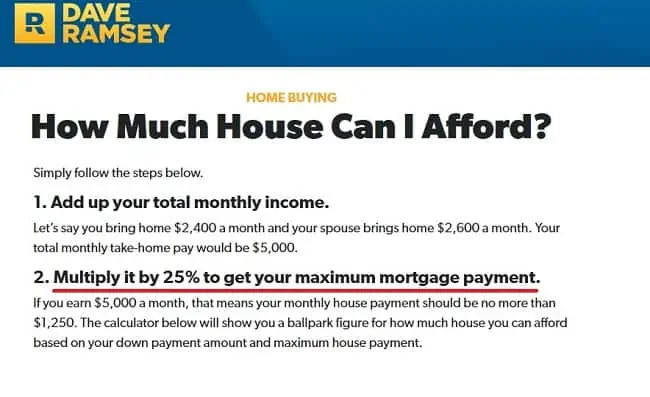

First, instead of using the 28% and 36% numbers, we’re going to say 25% of your monthly income is spent on housing and no more than 30% on total debt payments. This gives us that extra cash cushion and will help you avoid being house poor.

And there are two ways to approach this for finding the maximum monthly mortgage payment you can afford. You can either start with the 25% rule for your housing costs or the 30% rule for total debt. Whichever you use first, you’ll use the other rule to double-check to ensure you’re in a good place with your mortgage.

We’ll start off by adding up all your monthly debt payments. Include everything here, like credit cards, car loans, and personal loans. For credit cards, add up your monthly payments over the last year and divide by 12 to get a monthly average. That will help you avoid a big hole in your budget come Christmas.

Now a lot of your debt payments might only be temporary, so you might only owe another few years on the car loan, but you want to find out how much mortgage payment you can afford right now. If some debts drop off your budget in the future, that’s just going to mean you can save more, but you don’t want to over-extend yourself until they do.

After adding up all your monthly debt payments, multiply your monthly income by .3 or 30% to find how much you can afford. The difference between this number and your current debt payments is the mortgage payment you can afford.

How to Estimate Costs to Afford a Home

For example, let’s say you and your spouse make $5,000 a month. Thirty percent of that, or sixty grand times .30, would be $1,500 a month you can afford for total debt payments. If all your credit cards, car loans, and other debt are $700 a month, you can afford a mortgage payment of $800 a month.

Now we’re going to check that number against the rule for 25% of your income for housing costs to make sure we’re still safe. You see, sometimes those two rules are going to conflict a little. Maybe the 30% total debt rule says you can afford one payment while the 25% housing costs says another. You want to go with the lower mortgage payment here to make sure you’re not busting your budget and living on the edge each month.

So the 30% rule said we could afford an $800 mortgage payment. Now we add in an estimate for utilities, HOA fees, taxes, insurance, and maintenance to see if it will all be less than 25% of our income.

Of course, the problem here is we don’t know exactly how much these will be until we know which house we want to buy. I don’t want to make this any more complicated than it already is, though, so I want you to use the expenses you pay on your current home or your parents for right now. Then, when you find a home you want to buy, you can revisit the calculation with exact numbers to ensure it still comes out.

In our example, we were making $5,000 a month. That income times .25 or 25% tells us we want to spend no more than $1,250 monthly on housing costs. So if we’re looking at a mortgage payment of $800 from our 30% rule, we’d have $450 monthly for all those other expenses.

You can also use these two steps in the other order. Find how much monthly mortgage you can afford based on housing costs and the 25% rule before checking it against the 30% rule for total debt payments.

For example, if you make $6,500 a month then 25% of that would be $1,625 you could afford on monthly housing costs. If you estimate utilities, taxes, insurance, and other expenses will be $500 a month, you could afford a mortgage payment of $1,125 a month.

But let’s say you already have $1,000 in monthly debt payments. If we’re multiplying our $6,500 income by 30% then we don’t want total debt payments to be more than $1,950 a month. With a grand already, we need the mortgage payment to be $950 a month or less or we start getting into trouble.

I know it seems like a lot of numbers but play with it a few times. This will mean the difference between being financially stressed out for the next 15 years or being happy and confident you can pay the bills every month.

The Secret to How Much Home You Can Buy

Now I want to use this, along with Dave Ramsey’s mortgage advice for a secret savings trick you won’t even hear from Dave himself.

So Dave is the ultimate on debt discipline and he also recommends the 25% rule for your housing costs instead of the 28% rule. Where I disagree with him is Dave recommends only using a 15-year mortgage.

The idea is that a shorter-term mortgage will mean buying a less expensive house because you’re cramming all the mortgage payments into 15 years instead of 30. Rates on 30-year mortgages are at record lows, but it should be an excuse to spend more money.

So ready for that savings hack? When you’re talking to the bank or using a mortgage calculator to find out how much that mortgage payment you can afford, how much house that means you can afford, you’re going to look at it on 15-year loan terms. You’ll take the monthly mortgage payment you can afford, the one you found using the 25% and 30% rules, you’ll set in the mortgage calculator for a 15-year loan and see what total price you can afford on a home. This is your max price for buying a home.

But the savings hack here is that when you go to get a mortgage, you will be getting a 30-year loan. If you stay under the max price we saw on that 15-year loan, your monthly mortgage payment is going to be way lower. You’ll save hundreds of dollars a month and can invest that money for a higher return to build your nest egg.

Let’s look at an example here. If we find we can afford a $1,500 monthly mortgage payment. So if I plug these numbers into a home affordability calculator; we’ll use a 20% down payment so we don’t have to pay mortgage insurance each month, we’ll estimate a 5% interest rate and a loan term of 15 years. The front end and back end ratio, these are those rules we used for costs so we’ll use 25% in this first one and 30% in the second.

Now let’s say we make five grand a month plus three grand from our spouse’s earnings. We’ll say $910 a month in debt payments already from a car loan, student loans and cards. We’ll estimate property taxes at 1.2% and insurance at half a percent which are around the national average and hit calculate.

This is telling us we can afford a loan amount just under $195,000 with a $48,000 down payment and a home value of $243,300 which is going to mean payments of $1,540 a month.

Just as important here, notice down here where it estimates our front-end and back-end ratios. So with that payment, we’re only at 19% of our income to housing costs which is way under the 25% rule but we’re at 31% of our income in monthly debt payments. That’s just over our 30% limit but we should still be OK as long as we don’t go over these numbers.

Now if instead of that 15-year loan, we use a 30-year mortgage when we go to buy the house, so we can put the home value and mortgage amount in here. Home value at $243,300 and 20% down payment. We use the same 5% interest rate, the taxes and insurance estimates we used in the previous example and calculate our actual monthly payment.

So the actual payment on a 30-year mortgage here would be $1,388 a month, not the $1,543 we had on the 15-year loan. We’ve stayed within our budget using those 15-year loan terms and we have an extra $155 a month we can save and invest.

Risks to How Much Home You Can Buy

Now as you’re digesting all this, playing with the numbers, I need you to understand there are going to be some bad guys in the process.

The banks and real estate agents want you to buy as big as possible, to borrow to break the budget. The bank is going to ‘pre-qualify’ you for as much as you can possibly afford but it’s not taking into account saving for retirement. So when you’re running these numbers with the loan officer, he’s going to calculate your upper limit assuming you’re saving nothing and being a slave to that debt for the next three decades.

I worked as a real estate agent, first for commercial property then residential and I know how the game is played. Agents make their money on the sales price of the house. For every $10,000 more you spend, that agent is going to put another $700 in their pocket. This means you can’t rely on anyone else to tell you how much house you can afford.

Run through the numbers yourself, play around with it to find the price that’s within your budget but without making you miserable trying to make those payments.

You can afford a house but you need to know how much and how to negotiate the best price. From the percentage of income method to percentage of debt payments, you’ll be able to find how much house you can afford and still live comfortably.