Identity theft and personal loan scams are increasing as more of our lives go online. There’s big money in the billion-dollar personal loan business and even more in stealing people’s banking information.

Apart from completely unplugging your world and living the hermit life in the back woods, knowing some of the most common warning signs of personal loan scams is the best way to avoid being a victim.

Scammers quickly change their tactics, but these seven warning signs always seem to come out and give the fraud away.

Use these seven personal loan scam warning signs to protect yourself and check if a loan company is legitimate.

Personal Loan Scam Warning Sign #1: No Credit Check Loans

Online lenders are in the business of making loans and collecting interest as you repay these loans. They can only guess whether the borrower will repay the loan by looking at a borrower’s credit history.

Don’t believe any lender that says they have ‘breakthrough’ technology that can estimate your credit or the interest rate on your loan through other information like your answers to a survey or social media. Related to this, don’t trust lenders offering “no credit, no co-signer” loans.

Legit online loan companies will always want to do two checks on your credit report, a ‘soft’ inquiry and a ‘hard’ inquiry. The ‘soft’ inquiry is to verify some of your application information and doesn’t go on your credit report. They pull the ‘hard’ inquiry after you agree to the interest rate and before they fund your loan.

The only online loans that don’t require a credit check or where your credit score won’t matter are payday loans like Check into Cash. These loans are only for a week or two, and rates are so high that the lender makes money even if a few loans default.

I won’t say there’s no place for payday loans in your life. However, you might not have much choice if you have bad credit. Understand the few times when a payday loan is a better alternative and how to avoid the payday loan rate trap.

Recommended Safe Loan Sites:

These are the websites I have used for personal loans and the ones that come most recommended by readers as legitimate. You can find a full review of each later in this article.

- PersonalLoans – I’ve used this site twice for consolidation loans and home improvement. Great for poor credit borrowers.

- BadCreditLoans – Lower loan amount and shorter terms but will approve loans with a much lower credit score than other sites.

- Upstart – Generally need a higher credit score, but their unique scoring gives extra points (and lower rates!) to those with a college degree.

Personal Loan Scam Warning Sign #2: Upfront Fees or Loan Collateral

Upfront fees or loan collateral is the most common of personal loan scams. It used to be that scam lenders would ask you to wire an origination fee from your bank account to process the loan.

People got wise to this scam, so now scam lenders ask for debit card information to act as collateral on a personal loan. They say they aren’t touching the money on the debit card but want to know that there is money in the account for security on the loan.

Then they drain the debit card, and you never hear from them again.

You might pay a fee for a personal loan, but it will always come out of your loan when it is funded. If a company is so sure that it can get you a personal loan, why is it asking for money upfront?

Better yet, go with a personal loan lender that doesn’t charge a loan origination fee like PersonalLoans. Avoiding the origination fee, as high as 5% on other personal loan sites, can save you hundreds on your loan.

Personal Loan Scam Warning Sign #3: Unregistered Lenders in Your State

All personal loan companies and lenders must register in the states where they do business. Registration is usually done through the State Attorney General’s Office and helps the state monitor what financial promises are being made to the public.

Don’t believe a lender if they say they don’t need to register because they are solely online or are not a U.S. company. If they aren’t registered, they are either lending illegally or an outright scam.

It’s always a good idea to check your state’s Attorney General’s website for complaints on a lender anyway. Don’t blow this off. It only takes a few minutes which isn’t a lot of time when you’re talking about borrowing thousands of dollars.

Personal Loan Scam Warning Sign #4: No Physical Address

This personal loan scam warning sign isn’t quite as concrete as the others, but it’s a sound check and could save you when in doubt. Most lenders are going to have a corporate office building or at least a physical address. Even online lenders will have offices somewhere.

Check the lender’s address on Google Maps if you’re unsure about the company. This warning sign isn’t as definite because I’ve seen legit businesses where the address image on Google Maps was nothing more than an empty field. The warning sign isn’t perfect but be cautious of PO box addresses or non-existent offices.

Personal Loan Scam Warning Sign #5: Emails out of Nowhere

It always amazes me how spam email catches so many people every year. Any stranger offering you a commission, bonus, or any money in an email is 99.9% of the time a scam. So why are they contacting me and not someone with experience in this kind of thing?

These email scams happen in personal loans as well. You receive an email with a loan offer and a rate that is too good to turn down, along with a link where you can supply your personal information. If the scammer didn’t have malicious software in the link that hacks your computer, then the information you provide is more than enough to steal your identity.

Never click on a link or open an attachment in an email from someone you don’t know. Just don’t do it. It’s not a sweepstakes number or a hilarious cat picture. It’s a hacking scam to get your information.

Personal Loan Scam Warning #6: Misspellings, Capitalization, and Grammar

This scam warning would be funny if it didn’t still trap so many people into losing their money. If you can’t remember requesting information from a lender and don’t want to simply delete the email, make sure you read it carefully for grammar and spelling mistakes.

Many of these loan scams come from outside the United States, where English is not their native language. Scammers write a quick email in English and hit send to 10,000 recipients, hoping that at least a few will fall for the scam.

Hereis an actual loan scam email example I received that has quite a few warning signs.

Paypal scams are some of the most common because people can steal your money quickly, and it is more difficult to track than traditional bank accounts.

You’ll notice that there is no name after the “Dear,” Often, scammers will scrape a hacked website for information like names and email addresses. The emails they send populate areas like the name from the hacked info. There will be a blank space or a weird greeting if there is no name on the account.

There will also often be misspellings and grammar mistakes in these scam emails. But, of course, any company worth billions of dollars has enough money to check its emails.

Finally, loan scam emails almost always have a clickable button or link asking you to verify your information. What is happening here is the hackers are either putting a virus on your computer to steal your info or will ask you to ‘confirm’ your identity on the website. But, instead of confirming your identity, you will give them all the information they need to steal your money!

Personal Loan Scam Warning #7: Email Address

Here is another easy scam warning to spot but one that most people are aware of.

When you send an email from a website, the back half of that email address (the part after the @) will have the name of that company or website. So, for example, emails sent from Paypal will say @paypal.com, while emails sent from Gmail will say @gmail.com.

If an email says it’s coming from Paypal, but the address ends in anything other than @paypal.com, it is a scam.

Always double-check where the email is coming from before you consider reading it.

Common Loan Scams on the Internet

One of the most common loan scams is what’s called phishing. Phishing is where the scammer sends out thousands of emails to potential victims. The emails usually ask the recipients to confirm their bank account information when, in fact, they are giving the hackers all the info they need.

Another common loan scam is that the ‘lender’ will deposit into your bank account, supposedly to confirm the bank account for a future loan amount. They will then ask you to wire the money back to their account within 24 hours, and they can release your loan.

What ends up happening is the scammer waits for you to wire the money to them, then they cancel the first deposit made to your account. Unfortunately, it takes time for deposits to move from one account to another, so just because your bank account shows money coming in doesn’t mean that money is in your account yet.

This differs from the actual process of confirming a bank account used by most lenders. The lender will make two small deposits, almost always less than $0.50 each, and then ask you to confirm the amounts on their website.

They will withdraw the two deposits automatically after confirming the account, but a legitimate lender will never ask you to send the money back yourself.

How to Find Legitimate Loans on the Internet

We’ll cover what to do if you become the victim of a peer lending scam in the next section, but there are some things you can do to find legitimate loans on the internet.

Reading through some of the loan scam warning signs should give you an idea of how to find legitimate loans online.

- Always visit the lender’s website directly. Don’t click through an email to go to their site.

- Avoid loans that promise no credit check or that require upfront fees

- Make sure lenders are registered to do business in your state

- Ignore any emails for loans. Legitimate lenders rarely market by email, if ever. Most spend their marketing on advertising online or on TV.

It helps to read a few reviews of online lenders and find two or three that you might be able to qualify for a loan. This will mean knowing your credit score and the approximate credit score you need to get a loan from each lender.

Some sites only lend to borrowers with very high credit scores, while others will approve bad credit borrowers.

I’ve used several peer-to-peer lending sites and online lenders over the last ten years.

I started with PersonalLoans.com after destroying my credit score in the 2008 housing bust. I used the loan site to consolidate my debt and later for a home improvement loan. The site specializes in bad credit loans but offers several options, including p2p, personal loans, and even traditional bank loans.

- Credit score of 580 or above

- Loans up to $40,000 with monthly payments up to 60 months

- Rates from 9% to 36% depending on your credit score

Check your rate here on PersonalLoans.com

Upstart is a newer online lender with a unique credit scoring system that may make it easier for some borrowers to get a loan. Instead of just using your credit report and score to approve your loan, Upstart also considers your academic history, including your school and degree.

That makes the site perfect for newly graduated borrowers with no or little credit. It can be an excellent option to consolidate student loans or get the money you need to start your professional life.

- Credit score isn’t as important as on other sites

- Loans up to $50,000 with monthly payments of up to 60 months

- Rates from 9% to 30% depending on multiple factors

Check your rate here on Upstart

Online lenders will do a soft-pull of your credit when you apply, so it doesn’t affect your credit score. Then, only when you accept the loan does the site do a hard pull of your report, and the loan goes on as a debt.

The soft pull is why I recommend applying on at least two or three sites to see which one offers the best rate. Applying takes less than five minutes, and just a 1% difference can save you thousands on your loan.

Remember, you’re not only checking to make sure the loan company is legit but that you’re getting the best deal available. So if you can save just a few percent on your loan by spending twenty minutes comparing loan sites, isn’t it worth it?

How to Check if a Loan Company is Legitimate

Whichever loan company or personal loan provider you choose, you should always check to ensure it’s legit even if you get the name of the loan company from a friend or family member, especially if you get the name of the company from a friend or family member!

It’s because that’s how these personal loan frauds work, through word of mouth from friends and family. First, they pay out a small portion of the promised loans, which gets word of mouth, and then the scammers empty everyone’s bank account.

So always check to ensure a loan company is legitimate by checking its record with your state’s Secretary of State or Treasury website. They will have a page dedicated to loan scams and personal loan frauds where you can check for the loan company.

What to do if you become the victim of a personal loan or peer lending scam

If you are the victim of one of these personal loan scams, call your local police immediately to file a report. They likely won’t be able to do much if it’s an online lender, but it will get the report filed, and public and might help others in your area avoid the same scam.

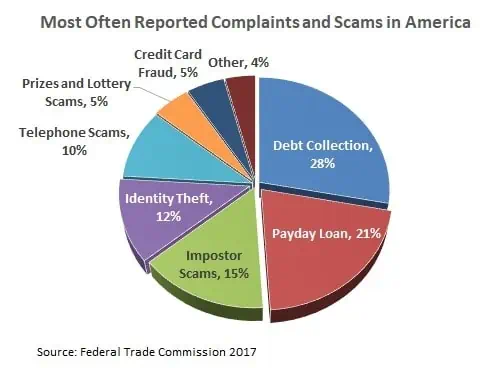

Next, file a complaint with the Federal Trade Commission (FTC) Internet Crime Complaint Center. Again, this isn’t so much to resolve the crime but to report it publicly and shut down the loan scammers.

You can also contact authorities in your state, usually the Attorney General’s office, about potential loan scams. It is essential to know the lending laws in your state. For example, payday loans are prohibited in North Carolina, Georgia, and many other states. Unfortunately, this sets the stage for a lot of scams and fraud against residents.

You also need to contact each of the three credit rating agencies; Experian, Equifax, and TransUnion. You must notify them by phone or in writing that your personal information may have been stolen. This will help your case if any charges are made to your credit accounts or your identity is used for new loans.

Finally, check your credit reports every few months after the incident or annually to ensure nothing is being added without your permission. Identity theft happens every two seconds in America and can cost you tens of thousands, besides what it can do to your credit score and the rate you pay on loans.

Unfortunately, personal loan scams and identity theft are on the rise and something we must try to avoid. The scammers are looking for easy targets, so they know the warning signs of a personal loan scam. Check out the legit personal loan sites in our list of lending sites, including the features and fees of each.